One of the largest Emerging Market ETFs owned by large funds (including the largest hedge fund in the world, Bridgewater) is the Vanguard Emerging Markets ETF (NYSE:VWO)…

VWO ownership – source: NASDAQ

As markets panic out of EMs this month, VWO is trading near 52 week lows…

VWO 52 week daily chart – source:finviz.com

As large fund holders start to report their Q4 2013 institutional ownership data (Oct-Dec) for the February deadline, we took some stats of the ones who have reported to date:

As of as of 1/31/2014:

| Total Reporting: | 197 |

| Shares Sold (75): | -3,675,983 |

| Shares Added (11): | 5,530,900 |

| Net Total: | 1,854,917 |

| Net Difference: | 33.54% |

Relatively speaking, a larger number of funds (75) have reduced their emerging markets exposure, but far fewer (11) added to their positions. However the funds that increased their positions actually added 33.5% more shares than the funds that have sold.

The reporting is as of December 30th 2013 – the month before the current sell off really took flight. So the question is, are the funds that are accumulating really smart to buy at a discount, or perhaps they are in trouble this month as their newly acquired EM positions are moving against them?

We would be inclined to believe the ‘distressed fund’ theory for 2 key reasons:

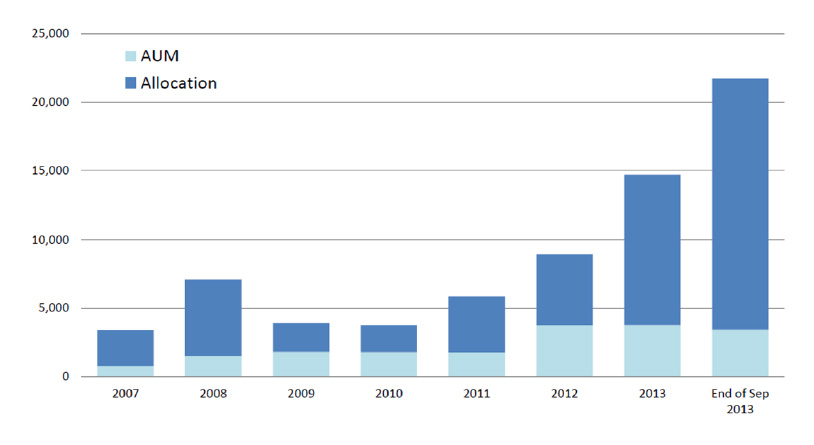

1. Hedge Fund leverage at all time highs: As per BAM (reported by Zerohedge), hedge fund buying power as a factor of assets is the greatest now since 2007. As we tweeted last week, it wouldn’t take much to push funds into de-leveraging mode, and therefore a sell-off in markets…

AUM vs. Buying Power

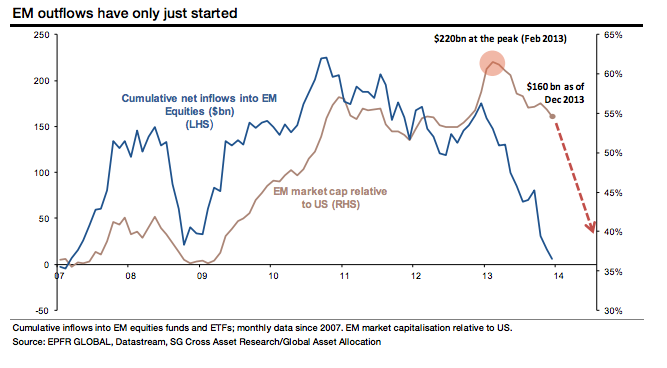

2. As SocGen has stated recently, outflows from EMs ‘have only just begun’ (as reported by FT)…

source: SocGen (via FT)

As FT reports, a number of funds could have simply ‘got it wrong’ in positioning themselves for a taper…

The notable difference with taper tantrum V.2, of course, is that US yields are compressing. Which might suggest that what the market got really wrong during taper tantrum V.1, was that a reduction in QE would cause a US bond apocalypse. This was a major misreading of the underlying fundamentals and tantamount to some in the market giving away top-quality yield to those who knew better. Taper at its heart is disinflationary for the US economy, and any yield sell-off makes the relative real returns associated with US bonds more appealing. That taper V.2 incentivises capital back into the US, at the cost of riskier EM yields, consequently makes a lot of sense.

So watch those treasury yields for clues.. if they stabilize, and even move lower, this could have implications for stocks which, rather than levitate into bubble territory, could chop around for the next year as risk normalizes and global capital flows catch up to reality.